Private

Privacy matters more than publicity.

Independent

My own research, tools, and judgment.

Resilient

Drawdowns, hardship, and recovery.

Current Standings

Live competition results from Financial‑Competitions.com — real-money accounts, independently verified. Past results tell part of the story; what matters just as much is keeping it going.

Algo & Discretionary

+11.73%

May 2026 Standing

$1M+ Enhanced Growth Division

Full portfolio account entered in the USIC Money Manager category: the Core Algo combined with discretionary positions. The complete picture of how I manage capital — personal funds only.

Financial‑Competitions.com — $1M+ Enhanced Growth

Active Trading

+33.67%

May 2026 Standing

USIC Enhanced Growth Division

Discretionary active trading account. Short-term position work, not the algorithmic long-term strategy — a different approach within the same competition framework.

Financial‑Competitions.com — USIC Enhanced Growth

Results are subject to audit and final verification by Financial‑Competitions.com.

Past verified result

US Investing Championship 2025

Real-money trading competition organized by Financial‑Competitions.com. Results audited against brokerage statements.

Financial‑Competitions.com ↗

+43.2%

Verified return

Real-money trading. Audited.

8th

$1M+ Enhanced Growth

Ranked in the top tier of the highest-stakes category.

Official certificate

View USIC 2025 certificate ↗

United States Investing Championship — audited result, $1M+ Enhanced Growth

Omar Abdul-Hameed

Who I am

Background

I am a money manager competing in the US Investing Championship, with decades of trading experience. My process combines a fully autonomous proprietary algorithm with discretionary judgment. I manage only my own capital — I do not offer this as a service to others.

As an inherently private and introspective individual, I value personal achievement and discretion more than public recognition. This site documents my approach, track record, and the thinking behind the tools I use.

Research and persistence

Living with a progressive medical condition, I have spent thousands of hours in research papers — not just for investing, but to understand my own health. That same analytical, relentless approach defines how I invest: unwilling to give up easily.

The ability to stay in a position through discomfort, to distinguish signal from noise, and to revise a view without abandoning a process — these are skills that transfer across domains.

Family and independence

I was partly raised by my grandmother, who gave me the warmth and stability I was missing elsewhere — and shaped much of who I am today.

I tend to be the trusted one in difficult times. That role has also taught me when to protect myself and how much to share.

How I invest

High risk, long-term capital growth — accepting deep drawdowns as part of the process, not as exceptions to it.

01

Pressure

Deep drawdowns and difficult periods are part of the reality, not exceptions to it. I focus on long-term capital appreciation rather than short-term stability, and tolerate strong volatility if the long-term thesis is intact.

I modelled behaviour across every major crash since 1957. The outcome was consistent: recovery is not exceptional. Capitulation is the only permanent loss.

02

Discipline

Research, structure, and judgment matter most when fear is highest. Some of my best trades came when I felt most afraid. Being scared is acceptable; acting with discipline despite fear is part of my edge.

I rely on my own research, tools, and judgment — not on outside opinions. The Core Algo runs autonomously, without interference, by design.

03

Recovery

Like a balloon pushed deep underwater, I tend to come back. I have recovered from levels where many would give up — in markets and in life.

I am drawn to the idea of returning stronger after hardship. The structure that survives pressure becomes the foundation for the next cycle.

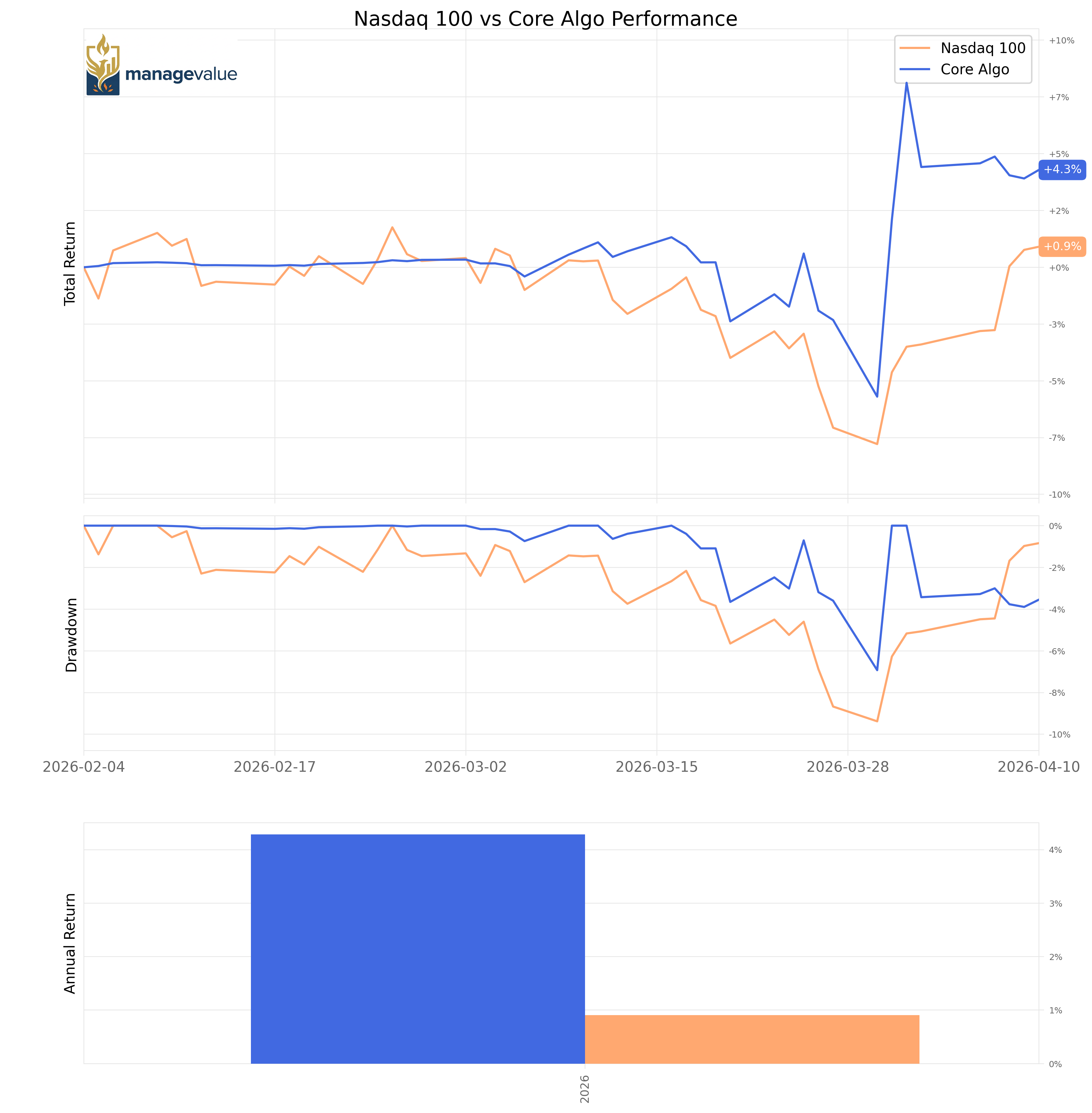

The Core Algo

Role in the portfolio

The Core Algo is the autonomous foundation of the portfolio — the base layer that handles all trading decisions by itself. It is not a rules overlay or a position-sizing tool; it is the entire decision engine, designed to run without discretionary interference.

It trades Nasdaq 100 stocks exclusively. Historical testing spans the Nasdaq 100 back to 1993 and the S&P 500 back to 1957 — stress-tested across the 1987 crash, dot-com collapse, 2008 crisis, COVID-19, and multiple stagflation and recessionary periods.

Fees stay low due to modest trading frequency, and slippage tends to balance out over time. I target a long-term net CAGR of roughly 30–50% per year.

Backtests

Results exclude slippage and fees — a theoretical tool, not a guarantee. The algo was tested on survivorship-bias-free data, validated on 5–10 year windows first, then applied to the full sample and cross-checked across indexes.

Backtests show exponential growth over decades, but live results differ. A six-month live run in 2025 confirmed the critical lesson: overriding the algo's signals degraded performance. The system must be allowed to run without interference.

Live Core Algo chart

Real live-trading results including fees and slippage, updated daily. The full portfolio is broader than this chart — it also includes discretionary positions beyond the algorithm.

Last updated 30th April 2026

As my discretionary trading has grown in size, I have had to block certain algo trades from executing in order to preserve margin stability across the full portfolio. This affects the performance shown in this chart, but has no bearing on the results reported through Financial‑Competitions.com, which are based on the audited account statements.

What this site is and is not

This site documents the work of a money manager who trades exclusively with personal capital.

I am not looking for investors and I do not manage capital for others. I am not licensed or registered to provide professional financial advice or money management services to third parties.

- Nothing on this website is personal financial, investment, tax, or legal advice.

- Nothing takes into account your individual objectives, situation, or needs.

- Nothing guarantees any outcome, result, or performance.

Investing and trading involve substantial risk. You can lose some or all of your capital. Past performance is not a reliable indicator of future results.

I value my privacy deeply. I may not always respond — please understand that discretion matters more to me than presence.

Contact notes

I sometimes write under pseudonyms — both in finance and in areas related to degenerative diseases — hoping to make life a little easier for others.

I respond when there is clear mutual value in the exchange.

Write to me

Sent via Formspree. No data stored on this site.